by Supreme Lending | Oct 17, 2024

Discover the Program Highlights of an FHA 203(k) Renovation Loan

Are you ready to turn a fixer-upper into your dream home? Whether it’s a home you’ve just bought or already own, renovation loans like the FHA 203(k) program may help you finance both the purchase and necessary repairs or updates all in one mortgage. Plus, the U.S. Department of Housing and Urban Development (HUD) announced that it is increasing the loan amount for Limited FHA 203(k) loans to $75,000 on all FHA case numbers effective November 4, 2024—that’s up from $35,000 which is huge news!

Here’s an in-depth look at how the FHA 203(k) renovation loan works, the differences between the Limited and Standard options, and what types of renovations may be covered.

What Is an FHA 203(k) Loan?

Insured by the Federal Housing Administration, the FHA 203(k) renovation loan allows homeowners to finance the cost of both the property and its renovations in a single loan. Whether you’re purchasing a home that needs updates or making repairs to your current home, this loan program may help make those dreams a reality. It offers the similar benefits of FHA loans for first-time buyers and repeat buyers alike. To qualify, eligible borrowers only need 3.5% down payment and there’s more lenient credit score requirements than other renovation loans.

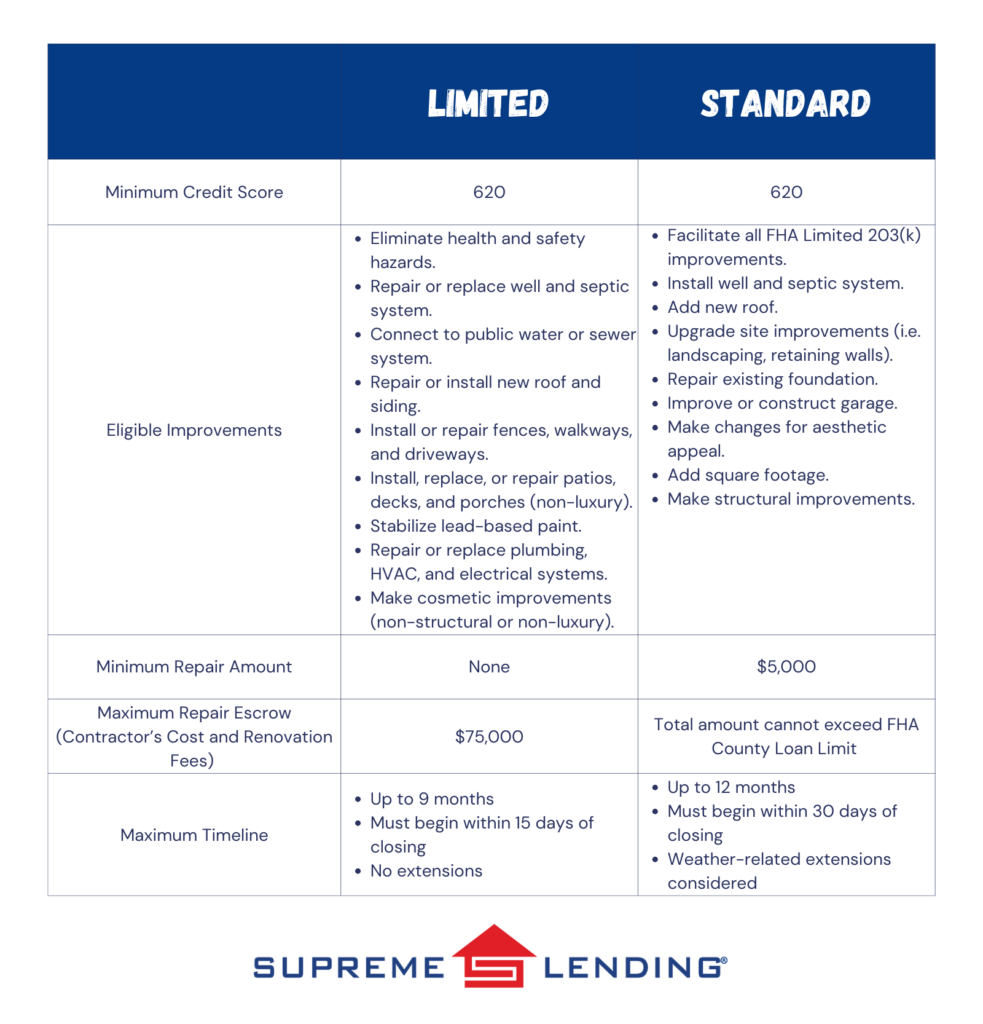

Limited vs. Standard FHA 203(k) Renovation Loan

There are two types of FHA 203(k) loans—Standard and Limited. Each has specific uses and limits depending on the scope of renovations you can make.

Limited FHA 203(k) Loan

The Limited 203(k) option is commonly used for smaller repairs and cosmetic upgrades. As mentioned, the loan amount will increase to $75,000 in November 2024, an exciting enhancement that will help open the door to renovations for more people. This loan covers non-structural projects such as remodeling kitchen fixtures, replacing flooring, painting, and minor landscaping. Unlike the Standard, the Limited program doesn’t require working with an HUD consultant or have a minimum loan amount.

Common Projects the Limited Covers

- Minor remodeling (i.e. updating kitchens or bathrooms)

- Replacing appliances or flooring

- Repainting or refinishing surfaces

- Energy-efficient improvements (i.e. installing new windows or insulation)

- Repairing roofs and gutters

Standard FHA 203(k) Loan

The Standard FHA 203(k) Renovation loan is more ideal for homes needing larger renovations and structural repairs. These may include adding rooms, replacing outdated plumbing or electrical systems, and fixing major structural issues. It has a minimum of $5,000 that must be used for renovations and the total loan amount must be within the FHA County Loan Limit. Because these projects are typically more complex, you’re required to work with an HUD-approved consultant.

Common Projects the Standard Covers

- Structural repairs or additions (i.e. adding on square footage or fixing foundation issues)

- Major systems replacements (i.e. plumbing, electrical, or HVAC systems)

- Roof repairs or replacements

- Modernization and improvements to the home’s function

- Accessibility improvements for people with disabilities

How Does the FHA 203(k) Renovation Loan Work?

The process for applying for an FHA 203(k) loan is similar to a regular FHA mortgage but comes with a few additional steps. Here’s an overview of how this loan program works.

- Find a property. Whether it’s a home you already own and want to refinance* or one you’re planning to purchase, identify a property that needs renovations.

- Get an appraisal. The home appraisal will assess both the home’s current market value as well as it’s “as-completed” value after the renovations are completed.

- Contractor and Estimates. Work with a licensed contractor to obtain the estimated costs for the repairs and improvements.

- Loan Application. You’ll apply for the loan based on the combined cost of the home and repairs.

- Renovation Timeline. Once the loan is approved, the renovation funds are placed into an escrow account and work begins. The renovation timeline can typically range from six months to one year.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

FHA 203(k) Combined with FHA 203(h) Disaster Relief Loan

Did you know that eligible borrowers affected by federally declared disaster areas may be able to combine the FHA 203(k) renovation loan with the FHA 203(h) disaster relief loan? This means adding the renovation costs into a new mortgage if your home was destroyed and deemed unlivable. Plus, the damaged property is eligible regardless of the age of the home. It only needs to have been a habitable residence prior to the disaster.

Ready to Rebuild?

At Supreme Lending, we understand how important it is to transform a home into one that truly meets your needs. Whether you’re fixing up a new property or renovating your current home, the FHA 203(k) renovation loan offers an excellent way to finance those improvements. We’re proud to offer both Standard and Limited options to fit the scope of your home projects.

Want to learn more about FHA 203(k) renovation loans or other mortgage options? Contact our team at Supreme Lending today and get pre-qualified!

Looking for other renovation loan options? Read more:

by Supreme Lending | Sep 20, 2024

Can repeat buyers qualify for FHA loans?

When you think of an FHA loan, it’s often associated with first-time homebuyers. After all, FHA loans are widely known for lower down payment and flexible credit requirements. But did you know that FHA loans are not just limited to first-time homebuyers? Insured by the Federal Housing Administration, FHA loans are available to anyone who meets the guidelines, including repeat buyers.

Whether you’re upgrading to a larger home, downsizing, or simply moving to a new area, FHA loans can still be a valuable mortgage option for eligible borrowers. However, there are some caveats. Let’s explore why repeat buyers may consider an FHA loan, how it works, and answer a few frequently asked questions.

FHA Loan Benefits for Repeat Buyers

Lower Down Payment

One of the key benefits of an FHA loan is the down payment requirement as low as 3.5% of the purchase price for qualified buyers. For repeat buyers who may have limited equity from a previous home sale or do not want to pay for a sizable down payment, this lower down payment may be appealing.

Flexible Credit Score

FHA are also known for their flexibility when it comes to a borrower’s credit score. While Conventional loans typically require a score of 620, the minimum for FHA loans is 580.

Competitive Rates

FHA loans often come with competitive interest rates, even for buyers who may not have top-tier credit. Locking in a lower rate may make a significant difference in the monthly mortgage payment and may result in potential savings over the life of the loan.

Assumable Loan

One of the most unique features of an FHA loan is that it’s assumable. This means that if you sell your home in the future, the buyer can essentially take over your FHA loan, including the rate, if they qualify. When you’re looking to sell the home, this could make the offer more attractive to potential buyers, especially if interest rates are higher than when you purchased the loan.

Gift Funds

FHA loans also allow mortgage gift funds to be used for 100% of the down payment or closing costs. In this case, family members or other eligible donors may give you the money to cover the upfront costs with no repayment obligation.

FHA Loans for Repeat Buyers: Frequently Asked Questions

Can non-first-time homebuyers use an FHA loan?

Yes, FHA loans are not reserved exclusively for first-time homebuyers. As long as the property is your primary residence and you meet the income, credit, and other qualifications, you may consider an FHA loan – regardless if it’s your first home or not.

Can FHA loans be used for second home or investment properties?

FHA loans are designed for primary residences only, which means you cannot use them to buy a second home or an investment property.

Can I have more than one FHA loan at a time?

In general, FHA only allows you to have one active FHA loan at one time. This is because the mortgage is designed for primary residences only. However, there may be exceptions such as relocating for work, a growing family, or having been a co-signer. Each situation is unique and requires proof to qualify for an exception. That’s why it’s important to work with a knowledgeable lender to go over your options.

Do FHA loans require mortgage insurance?

Yes, FHA loans require both an upfront mortgage insurance premium and ongoing monthly mortgage insurance payments. These payments help protect the lender in case of a default on the loan. Unlike private mortgage insurance for Conventional loans, FHA mortgage insurance premiums typically remain for the life of the loan unless you refinance into a non-FHA mortgage.

Ready to Take the Next Step?

The journey of homeownership doesn’t end after your first home purchase. Even if you’re not a first-time homebuyer, discover how FHA financing may still help open the door to your next home. Contact Supreme Lending today to get pre-qualified.

Related Articles:

by Supreme Lending | Jul 8, 2024

Learn about Supreme Lending’s BEYOND Program, an ITIN Loan Option.

Did you or someone you know just miss out on becoming eligible for a mortgage? Supreme Lending may have the solution with the BEYOND mortgage program, commonly known for being an ITIN loan option. However, it’s so much more than that!

Whether a gig worker, recent college graduate, or multi-generational family, the BEYOND program provides more opportunities for prospective homebuyers who may not yet qualify for an FHA loan. What is the BEYOND mortgage program, who can benefit from it, and how does it work? Read on to discover if this loan option could unlock the door to homeownership.

What Is Supreme Lending’s BEYOND Loan Program?

Essentially, the BEYOND program offers a lower down payment option for homebuyers who may be just beyond eligibility for an FHA loan, including non-permanent resident aliens with an Individual Taxpayer Identification Number (ITIN) or U.S. citizens and individuals who don’t have an established work or tax history.

Through this program, eligible borrowers can buy a primary residence with a purchase sales agreement. Then, they can refinance* down the road into direct ownership if they meet the qualifications in the future. This allows borrowers to get mortgage-ready while holding the equitable title interest.

Who Is the BEYOND Program Designed for?

Supreme Lending’s BEYOND program may be a good ITIN loan option for foreign national borrowers who do not have work authorization or a Social Security Number (SSN). However, ITIN borrowers are not the only people who may benefit from this unique loan program. Gig workers who may not have an established W2 income or newly self-employed people may qualify. Here’s an overview of borrowers who may be eligible for this program:

- Non-permanent resident aliens with an Individual Taxpayer Identification Number (ITIN); no work authorization or SSN required

- For example, ITIN mortgages typically require a higher down payment of 10-20%, so this program offers a more affordable ITIN loan option

- Deferred Action for Childhood Arrivals (DACA)

- 1099 or gig workers

- Borrowers who are relocating or awaiting citizenship

- Borrowers with a new job

- College graduates; deferred student loans do not need to be included in Debt-to-Income (DTI) ratio

- Multi-generational households

- Borrowers with credit issues preventing mortgage approval

How It Works?

- The first step of the BEYOND program is simply determining if the homebuyer qualifies. They will need to meet the program guidelines and get pre-approved for the purchase price limit based on income qualifications. An important starting point is to determine if the borrower has proof of successfully making rental payments within the last year. Several other criteria will also need to be considered.

- Once approved and the buyer makes an offer to buy a qualified property, they’ll enter into a sales contract. The contact is then assigned to a third-party government entity approved by the U.S. Department of Housing and Urban Development (HUD) to purchase the home as an investment.

- The buyer must pay at least a 3.5% down payment along with additional administrative fees.

- An FHA appraisal and home inspection are required.

- The government entity buys the home using an FHA loan.

- The homebuyer also signs a seller-financing agreement with the third-party entity, which gives them a recorded equity interest in the property. This agreement acts similar to a standard mortgage or deed of trust.

BEYOND Loan FAQs

What Proof of Rental History Is Accepted?

A key requirement is for the borrower to provide proof of successfully paying rent for the past year. This could be through checks, money orders, or reviewing bank statements. Living for free with family members will not qualify.

Are There Credit Requirements?

For ITIN borrowers, no credit score is required. For non-ITIN borrowers, a minimum credit score of 600 is required.

What Form of Identification Is Needed?

The borrower will need to present two forms of unexpired government-issued identification. One must be a picture ID (i.e. driver’s license or passport). ITIN borrowers must provide proof of ITIN documentation. Valid IDs from other countries are accepted.

What Upfront Costs Are Required?

Qualified borrowers will need to pay at least the minimum down payment of 3.5% along with program administration fees and the first monthly payment.

Does the Borrower Own the House?

They will have equitable title interest, which is legal ownership. This means borrowers can benefit from any equity gains. However, the title of the home hasn’t been fully transferred. Additionally, for borrowers who do qualify on their own in the future, the loan may be refinanced* into the borrower’s name and have the title transferred.

Homeownership In Reach

With programs like BEYOND, Supreme Lending is committed to providing affordable, flexible mortgages for all. Contact your local branch to see if you may qualify and take the leap into homeownership.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

by Supreme Lending | Jun 10, 2024

When it comes to financing your new home, choosing the right mortgage is so important – FHA loans, Conventional mortgages, down payment assistance – there are several options to choose from. Each loan program has its own set of guidelines, benefits, and considerations. Comparing loan types can help you make an informed decision of what may fit your needs and homeownership goals. Let’s examine the difference between these two popular options: FHA loans and Conventional mortgages.

What Is an FHA Loan?

FHA loans are mortgages insured by the U.S. government’s Federal Housing Administration (FHA) against borrower default. They are designed to help more people who may not qualify for Conventional loans achieve homeownership. Here are some key benefits of FHA loans:

- Lower Credit Score Requirements. FHA loans typically require a minimum credit score of 580, which is lower than Conventional loans.

- Low Down Payment. One of the most attractive highlights of FHA loans is the low down payment requirement. Qualified borrowers can put down as little as 3.5% of the purchase price, plus there may be options to include down payment assistance.

- Flexible Debt-to-Income (DTI) Ratio. FHA loans allow higher DTI ratios, making it more feasible for borrowers with existing debt to qualify.

- Assumable Loans. FHA loans are assumable, meaning if you sell your home, the buyer can take over your existing FHA loan. This could potentially help save buyers money on closing costs and interest.

- More Lenient Qualification Requirements. In general, the qualification criteria for FHA loans is more moderate compared to Conventional loans. This helps a broader range of borrowers become homeowners.

What Are Conventional Loans?

Conventional mortgages are loans not insured or guaranteed by any government agency unlike FHA. They are offered by private lenders. Borrowers typically need to have a higher credit score and lower DTI ratio.

- Lower Mortgage Insurance Costs. While FHA requires mortgage insurance premiums (MIP) for the life of the loan, Conventional loans typically only require private mortgage insurance (PMI) until the borrower buys down 20% of the mortgage.

- Higher Loan Limits. Conventional loan borrowers can generally qualify for higher loan limits compared to FHA. This can help borrowers purchase more expensive homes.

- Variety of Loan Terms. Conventional mortgages offer a wide range of loan terms and options, including fixed-rate and adjustable-rate mortgages (ARMs), providing more flexibility.

- Potential for Lower Interest Rates. Borrowers with higher credit scores and larger down payments can often secure lower interest rates with Conventional loans than FHA.

- Conforming & Non-Conforming Options. Conforming conventional loans meet the guidelines of government-sponsored enterprises (GSE), such as Fannie Mae and Freddie Mac. While non-conforming loans do not and can have higher loan amounts, including Jumbo loans.

Frequently Asked Questions About FHA vs. Conventional Loans

Which loan is better suited for first-time homebuyers?

FHA loans are often a great option for first-time buyers due to their lower credit score and down payment options. They provide a pathway to homeownership for those who may not initially qualify for a Conventional loan.

Can I refinance* my FHA loan into a Conventional mortgage?

Yes! Borrowers can refinance an FHA loan into a Conventional one. This could potentially eliminate the FHA’s mortgage insurance requirement if you have enough equity in the home and lead to more flexible terms.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.

Are there income limits for FHA or Conventional?

FHA mortgages don’t have income limits, but they may have loan limits based on the location of the property. Conventional loans don’t have income limits either, however higher income and a better credit profile can help you qualify for a larger loan amount.

How do I decide which loan is right for me?

Take into concentration your credit score, funds you have for down payment and closing costs, and long-term goals. FHA can be ideal for those with lower credit scores, while Conventional loans may be better suited for borrowers with stronger credit profiles. Getting pre-qualified with Supreme Lending can help give you estimated costs for each option.

Whether you opt for an FHA loan or a Conventional, both options provide pathways to owning your dream home. It’s important to review your current situation, consider the benefits of different loan types, and work with a knowledgeable loan officer to help guide you through the mortgage process.

At Supreme Lending, we’re committed to helping you navigate the homebuying process with ease. Contact your local branch to get started today!

by Supreme Lending | May 9, 2024

Learn why FHA loans may be a perfect option for first-time buyers.

While first-time buyers are hunting for their perfect home, they’ll also need to be on the hunt for the perfect mortgage—which may seem more overwhelming and not as enjoyable as touring properties. There are several financing options to choose from and programs available. It’s all about finding the one that fits best. At Supreme Lending, our goal is to provide the guidance you need to make informed decisions and be confident with your loan choice.

In this article, we’re highlighting a mortgage option that is designed specifically to help first-time buyers, FHA loans. Discover the many FHA loan benefits and why this option may be right for you.

Understanding FHA Loans: A Brief Overview

First, what exactly is an FHA loan? The Federal Housing Administration (FHA), a branch of the U.S. Department of Housing and Urban Development (HUD), insures FHA loans, which are issued by approved lenders. This insurance protects lenders against losses if a borrower defaults on their loan, making FHA loans less risky for lenders and consequently more accessible to first-time buyers.

FHA Loan Benefits

1. Low Down Payments.

To help overcome one of the biggest barriers for first-time homebuyers, FHA loans typically require a lower down payment compared to Conventional loans. This makes homeownership more accessible to people who may not have substantial savings or want to pay less upfront costs.

2. Flexible Credit Requirements.

FHA loans are more lenient when it comes to credit, allowing borrowers with lower credit scores to qualify for financing, which is beneficial for those who are still establishing their credit history. See common credit score and down payment requirements here.

3. Assumable Loans.

What does this mean? FHA loans are assumable, which means that if you sell your home, the buyer can take over your FHA loan, potentially offering them a competitive advantage in a rising interest rate environment. Restrictions on assumability may apply.

4. Lenient Debt-to-Income (DTI) Ratios.

DTI compares a borrower’s debt to their monthly income to measure’s their ability to manage monthly mortgage payments. FHA loans often allow for higher debt-to-income ratios compared to Conventional loans.

5. Lower Mortgage Insurance Premiums.

While FHA loans require mortgage insurance premiums (MIP), the premiums are often lower than those of Conventional loans, especially for borrowers with lower credit scores or smaller down payments. In fact, the FHA annual mortgage insurance premium was lowered from 0.85% to 055% in 2023 for most borrowers.

6. Seller Closing Cost Assistance.

Another benefit buyers could take advantage of is negotiating seller concessions to help cover upfront costs. FHA loans can allow sellers to contribute up to 6% toward the buyer’s down payment, appraisal fees, or other associated closing costs.

7. Gift Funds.

Gift funds are given to someone with no expectation of repayment, for example parents gifting their newlywed children money for a down payment. FHA loans allow borrowers to use gift funds from family members or other eligible sources to cover their down payment and closing costs. Note: A gift letter is required to confirm the gift funds.

8. Renovation Loans.

The FHA 203(k) Renovation loan is a home rehabilitation financing option, which allow borrowers to finance both the purchase price of the home and the cost of eligible renovations or repairs into a single loan. This helps buyers afford any necessary improvements and can open their home search to consider fixer-uppers.

9. Streamline Refinancing.

FHA loans offer a streamlined refinancing option, known as the FHA Streamline Refinance. This allows borrowers to refinance their current FHA loan with minimal paperwork and documentation, saving time and money.

10. No Prepayment Penalties.

FHA loans do not have prepayment penalties unlike some traditional mortgages. This allows borrowers to pay off their mortgage early without facing additional fees or charges, which can save money on interest over time.

11. 100% FHA Financing Available.

Did you know Supreme Lending offers two competitive FHA 100% financing options? Through the Chenoa Fund or the Supreme Dream program, these include a 30-year fixed-rate FHA loan paired with a second forgivable loan to be used toward down payment, closing costs, and prepaids.

These benefits make FHA loans an attractive option for first-time homebuyers, offering accessibility, flexibility, and affordability to achieve homeownership.

Ready to get started? Contact Supreme Lending today to learn more about FHA loans or other mortgage services we offer.