by Supreme Lending | Nov 9, 2024

You’ve submitted your initial mortgage application, completed the necessary paperwork, and even had your home appraised. Now, you find yourself at the crucial stage of the loan process – underwriting. This is where the underwriter, acting as a gatekeeper for the lender, meticulously assesses your financial details to determine the risk of financing your home. In this article, we will explore the mortgage underwriting process, its significance, and what borrowers can expect during this critical phase.

Who Are Underwriters and What Do They Do?

Underwriters play a pivotal role in safeguarding the interests of the lender during the home loan process. Their primary responsibility is to assess your ability to repay the loan and evaluate the risk associated with lending money to you. They review various aspects of your financial profile, including your credit score, income, and the appraised value of the property. The goal is to ensure that borrowers are not taking on more mortgage responsibility than they may be able to handle.

Importance of Underwriting:

The housing crisis of 2008 highlighted the need for stricter underwriting guidelines. Loose regulations during that period allowed borrowers to access funds without adequate means to repay, resulting in widespread defaults. Today, underwriters adhere to stringent guidelines to help prevent the recurrence of such crises, protecting both borrowers and lenders alike.

What to Expect During the Underwriting Process:

Further Paperwork May Be Needed:

During the underwriting process, underwriters may request additional documentation to gain a comprehensive understanding of your financials. It’s crucial to provide any requested documents promptly to keep the mortgage process moving smoothly.

Turn-times Vary:

Depending on the loan type and market conditions, the underwriting process may take anywhere from 5 to 14 days. Understanding the potential timeline may help you manage expectations and plan accordingly.

Disclosure Mailings:

Borrowers may receive electronic or paper loan disclosures throughout the process. These disclosures are sent to ensure compliance with state and federal laws.

Loan Determinations:

After reviewing your application, the underwriter will issue one of three determinations:

Conditional Approval of Loan:

Your loan is cleared for funding, and your lender will discuss any remaining conditions specified by the underwriter. A closing date will be scheduled.

Suspension of Loan:

A suspension occurs when there are questions about a critical facet of your loan file. Your lender will work with you to identify and address any concerns, leading to a potential conditional approval.

Denial of Loan:

If your file indicates a high level of risk, the underwriter may deny the loan based on industry benchmarks, not personal intuition. For example, perhaps there was a significant drop in your credit score, indicating potential payment inconsistencies and a big risk for a lender.

What Happens If Your Loan Is Suspended or Denied?

Choosing the right lender is crucial, and at Supreme Lending, the relationship doesn’t end if your loan faces challenges. Supreme’s dedicated team may be able to help overcome underwriting objections, identify errors, and work with you to improve your application.

Understanding the mortgage underwriting process is vital for borrowers navigating the complex world of home loans. As you approach this final checkpoint, being prepared for potential requests for additional documents, varying turn times, and the possible outcomes of the underwriting review can help streamline the process. With Supreme Lending by your side, you can navigate the underwriting process with confidence and increase the chances of a successful loan closing.

Dos and Don’ts During the Mortgage Underwriting Process

The journey to homeownership involves various stages, and one of the most important steps is the mortgage underwriting process. This phase determines whether your loan will be approved or not. To ensure a smooth underwriting experience with Supreme Lending, it’s essential to follow a set of Do’s and Don’ts.

Do’s:

Maintain Consistent Debt Payments:

Make minimum monthly payments on your consumer debt until the loan closes. Any deviation from this may have adverse effects on your mortgage application.

Timely Mortgage Payments:

Ensure your mortgage payments are made on time and are no more than 15 days late. Any delay beyond this timeframe may pose risks to your loan approval.

Cooperate with the Title Company:

Respond to calls from the Title Company. Occasionally, there may be outdated or unreleased liens, which can complicate the ownership of your property. Addressing these issues promptly is vital for clearing your property’s title in preparation for closing.

Submit Requested Documents Promptly:

Provide any documents requested by Supreme Lending immediately. Timely submission is crucial, as documents can have expiration dates, and delays may affect your application.

Retain Financial Documents:

Hold onto electronic and paper copies of pay stubs, bank statements, and other financial documents until the loan closes. You may be required to provide them during the underwriting process.

Don’ts:

Avoid Job Changes or Retirement:

Refrain from resigning or retiring during the loan process without consulting your Supreme Lending mortgage expert. Changes in employment status may impact your loan approval.

No New Credit Accounts:

Do not open or apply for new credit accounts before your mortgage loan closes. New accounts or inquiries can be easily identified during underwriting and may jeopardize your application. Our experienced professionals understand that life happens, and should a need arise for situations such as applying for student loans or financing a child’s upcoming college tuition, we ask that you discuss your plans with a member of our team before you take action.

Avoid Balance Transfers:

Refrain from making balance transfers on existing credit card balances. Such actions may slow down the mortgage application process.

Don’t Pay Off Existing Credit Accounts in Full:

Avoid paying off existing consumer credit accounts (e.g. auto loans, credit cards, etc.) in full unless it aligns with the natural progression of making minimum monthly payments.

Successfully navigating the mortgage underwriting process requires careful attention to detail and adherence to specific guidelines. By following the Do’s and Don’ts outlined above, you may increase the likelihood of a smooth and successful loan approval. If you have any questions or concerns about your loan, don’t hesitate to reach out to the Supreme Lending team for assistance. Remember, open communication and timely action are key to a positive mortgage underwriting experience.

by Supreme Lending | Nov 7, 2024

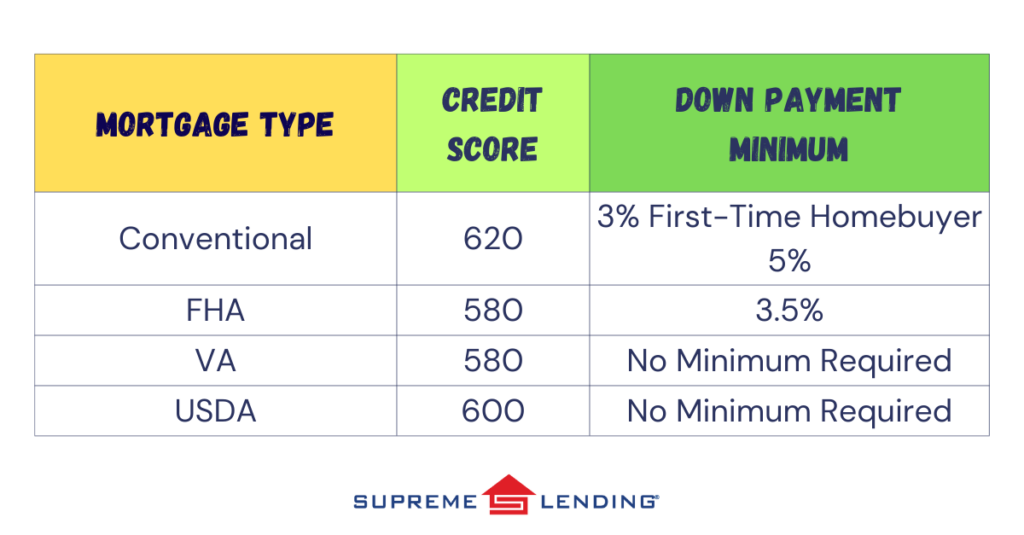

For aspiring homeowners and first-time buyers, many questions can arise about the mortgage process. What credit score do you need to qualify? How much down payment is required? Answers are based on several factors including the property, purchase price, and, most importantly, the mortgage type.

Here’s a breakdown to simplify the numbers and help you understand what you need to open the door to your dream home depending on common mortgage types:

What Is a Credit Score?

Commonly determined by FICO® score, credit scores are calculated using the borrower’s financial background information such as payment history, credit utilization, length of credit history, types of credit in use, and recent credit behavior. The average credit score in the United States in 2023 was 715, according to Experian data.

Down Payment Assistance Options

If a homebuyer doesn’t have the required minimum down payment or would like to access more financing, Supreme Lending offers several down payment assistance options for qualified buyers. This can also help first-time buyers open the door to homeownership. Guidelines and eligibility vary depending on the program. For example, the Supreme Dream program offers down payment assistance in the form of a fully forgivable second loan and requires a minimum credit score of 620. Ask your Supreme Lending Loan Officer about qualified assistance programs.

Understanding credit score and down payment requirements for different types of mortgages is crucial for prospective homebuyers. While each loan type has its own guidelines, maintaining a good credit score and having sufficient funds for upfront costs at closing remains a common denominator for securing favorable terms and interest rates. By proactively managing your credit and staying informed about your options, you can navigate the mortgage process with confidence on your journey to homeownership.

Contact your local Supreme Lending branch to get pre-qualified and learn about your home financing options.

by Supreme Lending | Nov 1, 2024

There are several important steps involved in the homebuying process, and an independent confirmation of the property’s value is a key step for mortgage approval. This evaluation is typically known as an appraisal. What is an appraisal, why is it done, and what else do you need to know about the appraisal process as a prospective homebuyer? Here are the basics.

What’s an Appraisal?

For those who have never been through the mortgage process before, an appraisal refers to an unbiased estimate of a home’s value. A professional appraiser evaluates the property to confirm its worth, which is then used to determine how much money can be loaned to the borrower through a mortgage.

In nearly all home purchases today, lenders require an appraisal before approving a loan. This is because they want to be confident that they’re not loaning more money than the property is worth, as this would put them at risk of loss if the borrower defaults on the loan.

Generally, appraisals are completed and filed within the jurisdiction in which the property is located. This is important to keep in mind if you’re considering a purchase in another city, county, or state, as different jurisdictions have different requirements and processes.

Why Are Appraisals Important?

As mentioned, appraisals play a vital role in the homebuying process as they provide an unbiased estimate of a property’s value. This number becomes incredibly important when negotiating a purchase price, as it can help confirm or refute the asking price set by the seller.

If you’re planning to obtain a mortgage to finance your home purchase, the appraisal value will also be used to determine how much funds you’re eligible to borrow. In some cases, the appraised value may be lower than the agreed-upon purchase price, meaning that the buyer would need to come up with the difference in cost.

Of course, it’s important to remember that appraisals may not always be 100% accurate. There is some subjectivity involved in the process, and different appraisers can sometimes come up with different values for the same property. That’s why it’s important for buyers to be aware of recent comparable sales in the area, as this can help them gauge whether or not an appraisal is fair.

What Do Appraisers Look for?

When an appraiser is assessing a property, they’ll be looking at several different things. Here’s a general list:

- Interior and exterior inspection: The appraiser will visit the property and conduct a thorough inspection, taking note of both the condition of the property and any features or amenities that may impact its value. This will cover both the interior and exterior of the property.

- Review of recent sales: The appraiser will also review recent sales of comparable properties in the area to get an idea of the current market value. These will be included in the appraisal report for review, along with a street map that shows the locations of those properties.

- Assessment of the property’s condition: The appraiser will also provide their opinion on the condition of the property, which can impact its value. Therefore, it’s important for sellers to make necessary repairs or improvements before putting their home on the market.

- Square footage calculation explained: Assessing square footage is another essential part of the appraisal process. The appraiser will determine the total square footage of the property as well as the livable space. This can sometimes be tricky, as there are different ways to measure square footage and some methods may result in a larger number than others. For this reason, appraisers are generally required to also include the method they used in determining the home’s square footage on the report.

- Photos: One of the most important parts of the appraisal report is the photos that the appraiser takes during their inspection. These provide a visual record of the property’s condition and can be helpful when reviewing the report.

The appraiser’s findings are presented in reports that typically are several pages and include other important information, such as the appraiser’s qualifications, contact information, and any licenses or certifications they may have.

Who Pays for Appraisal Costs?

Generally speaking, appraisals can run between $300-$700 for single-family homes, though the exact cost will depend on the appraiser and the property being assessed. In most cases, the buyer is responsible for covering the cost of the appraisal, though there are some instances where the seller may agree to pay. Homebuyers may have the option to roll the appraisal cost into their closing costs or possibly the mortgage itself.

For more information on the appraisal process, or to learn more about any of our mortgage products and services, contact your local Supreme Lending team today.

Related Articles:

by Supreme Lending | Mar 15, 2024

When considering buying a home, it’s highly recommended that the first step in your homeownership journey is to work with a lender to get pre-qualified or pre-approved for a mortgage. While the two terms sound similar and both help give buyers an understanding of how much they may qualify for a loan, there are distinctions between getting a mortgage pre-qualification and pre-approval. Let’s dive into the differences between these crucial first steps and benefits of each in your homebuying experience.

Mortgage Pre-Qualification: A Preliminary Evaluation

Pre-qualification is an early step in the homebuying and mortgage process. It offers buyers and lenders alike a high-level snapshot of a borrower’s finances and potential buying power. When getting pre-qualified, lenders will typically collect basic financial information provided by the buyer, including income, debts, assets, and any amount of savings or cash they may have available for a down payment. It’s a valuable starting point, giving you an idea of your budget before you start house hunting.

During the pre-qualification process, borrowers may be able to opt for a soft pull credit inquiry. This means your information would remain confidential, with no impact on your credit score and avoids unwanted credit solicitations and third-party trigger lead calls. Ask your loan officer about your credit reporting options.

While a mortgage pre-qualification is less detailed than a pre-approval, this step can be quicker and involves less documents to help busy homebuyers hit the ground running and start their home search. A pre-qualification letter can also show sellers your interest in buying a home and that you can afford an estimated mortgage.

Mortgage Pre-Approval: A Deeper Dive

A mortgage pre-approval takes a more detailed approach and provides an even clearer, more accurate picture of a borrower’s finances and capacity for a mortgage. This is because the loan estimate is based on validated details.

In this step, prospective homebuyers will need to provide their lender with thorough documentation of their financial history for verification, including records like pay stubs, tax returns, and bank statements. Lenders will also run the borrower’s credit score and verification of employment if applicable.

Once pre-approved, the borrower will receive the estimated loan amount they may qualify for based on the verified information—verified being the key differentiator between a pre-approval and a pre-qualification. A pre-approval also gives you, the buyer, a more competitive edge because it demonstrates to sellers that you’re serious and eager to buy a home.

Other Reasons to Get Pre-Qualified or Pre-Approved

- Determine Affordability. It gives you an idea of how much you can afford based on your credit, income, debt, and potential down payment funds. This will help guide your home search within your budget.

- Understand Monthly Payments. With the estimated loan amount you can qualify for, you can get a breakdown of your monthly principal, interest, taxes, and insurance costs to help set expectations for planning your mortgage.

- Find the Right Loan Program. Evaluating your financial details and knowing how much you can qualify for can also help you determine the loan type best fit for your needs and if you could benefit from programs such as first-time homebuyer or down payment assistance.

- Strengthen Your Offer. As mentioned, having a pre-qualification or pre-approval can show sellers you’re a credible buyer and strengthen your offer on a home, which is especially helpful in a competitive market.

- Save Time. Being prepared in advance with a pre-qualification or pre-approval helps identify and avoid any potential roadblocks that could arise during the mortgage process, setting you up for a smooth closing.

In conclusion, getting a mortgage pre-qualification or pre-approval offers invaluable knowledge and opportunities in your homebuying journey. Ready to take the first step? Our Supreme Lending loan officers are ready to serve you! Contact your local branch today.

by Supreme Lending | Mar 13, 2024

The decision to refinance* your mortgage is a strategic move that can have a profound impact on your financial well-being. There are several types of situations when refinancing might provide specific benefits and unlock potential savings. It’s important that homeowners have a clear idea of the possible outcomes when considering a refinance. Let’s dive into a few of the most common reasons people may refinance, some of which may apply to your situation.

Getting a More Favorable Mortgage Rate

A key reason that homeowners refinance is to get a more favorable mortgage interest rate. This can be done by either securing a lower interest rate than your current mortgage or by switching from an adjustable-rate mortgage (ARM) to a fixed-rate loan. In both cases, this may lead to significant savings over the life of the loan and may even reduce the monthly mortgage payments.

When mortgage interest rates drop lower than your current loan, it’s important to note that there are several additional considerations to be aware of, including fees and upfront costs associated with refinancing as well as the amount of time left on your current loan. Working with a trusted lender that provides personalized, transparent refinancing details and costs will help you make an informed decision for your mortgage needs.

Changing the Terms of Your Loan

Another common reason people refinance is to change the terms of their loan. This may involve extending the length of the loan to lower monthly payments or shortening the loan term to pay off the mortgage quicker. Refinancing to a shorter-term loan may increase your monthly mortgage payment, so it’s important to consider your budget before making this decision.

Switching Loan Type

Some homeowners may refinance to opt for another loan type, for example moving from an ARM to a fixed-rate mortgage. Interest rates—and subsequently monthly mortgage payments—for an ARM can increase or decrease based on market conditions, so borrowers may be more comfortable switching to a fixed-rate mortgage that has a steady interest rate and monthly payment that won’t change.

Another scenario could be borrowers wanting to change from a government loan, such as FHA or VA, to a Conventional mortgage. This could be an effective way to save on some loan costs by removing required fees typically associated with government loans.

Removing a Co-Signer

If you required a co-signer to qualify for a mortgage, you may be able to remove them from the loan by refinancing after improving your eligibility to qualify for a loan by yourself. Not only does this free up the co-signer from their financial obligation, but it may also help you qualify for a lower interest rate on your loan, especially if your credit score improves when the co-signer is removed. This could lead to more favorable loan terms. Homeowners may also want to remove a co-signer in the event of a divorce resulting in one spouse assuming sole ownership of the home and full responsibility for the mortgage.

Removing Private Mortgage Insurance or Mortgage Insurance Premium

For those who put down less than 20% down payment for a home, a common requirement is carrying private mortgage insurance or PMI. This protects the lender in case the borrower defaults on the loan, but it also means an additional monthly cost that can add up over time.

With Conventional mortgages, you don’t have to always refinance to remove PMI. It can be removed after you’ve reached a certain equity threshold in the home—usually 20%. However, some mortgage programs, like FHA loans, require a Mortgage Insurance Premium (MIP) for the life of the loan. An FHA borrower would need to refinance to a Conventional mortgage to remove the MIP cost.

Cashing Out Equity

Finally, another popular way homeowners utilize refinancing is to cash out the equity that’s built up in the home. If you refinance an amount greater than what you owe on your home, you can receive the difference in a cash payment to be used as you wish. For example, you may use this cash to fund home improvements, pay off high-interest debts, or for other large expenses. How you use the cash is up to you.

It’s important to remember that cashing out equity will increase the amount you owe on your home and may also lead to a higher interest rate—factors that should not be overlooked.

As you can see, there are a variety of reasons why homeowners may choose to refinance their mortgage. It’s important to carefully consider your individual circumstances and financial goals before making a decision, as refinancing may not be right for everyone.

For more information on reasons to refinance, or to learn more about any of our mortgage programs and services, reach out to your local Supreme Lending team or contact us today.

*By refinancing an existing loan, total finance charges may be higher over the life of the loan.